Preparing for the CPA exam requires more than reading notes. Texam is structured around distinct sections that test different areas of accounting knowledge, from auditing and financial reporting to tax compliance and information systems. Understanding how the exam is organized is just as important as mastering the material itself.

Below, I created section-specific practice questions designed to reflect the scope and structure of the CPA exam. Each group is organized by topic area so you can focus your study time intentionally and work through material in a way that mirrors the actual exam experience.

Key Takeaways

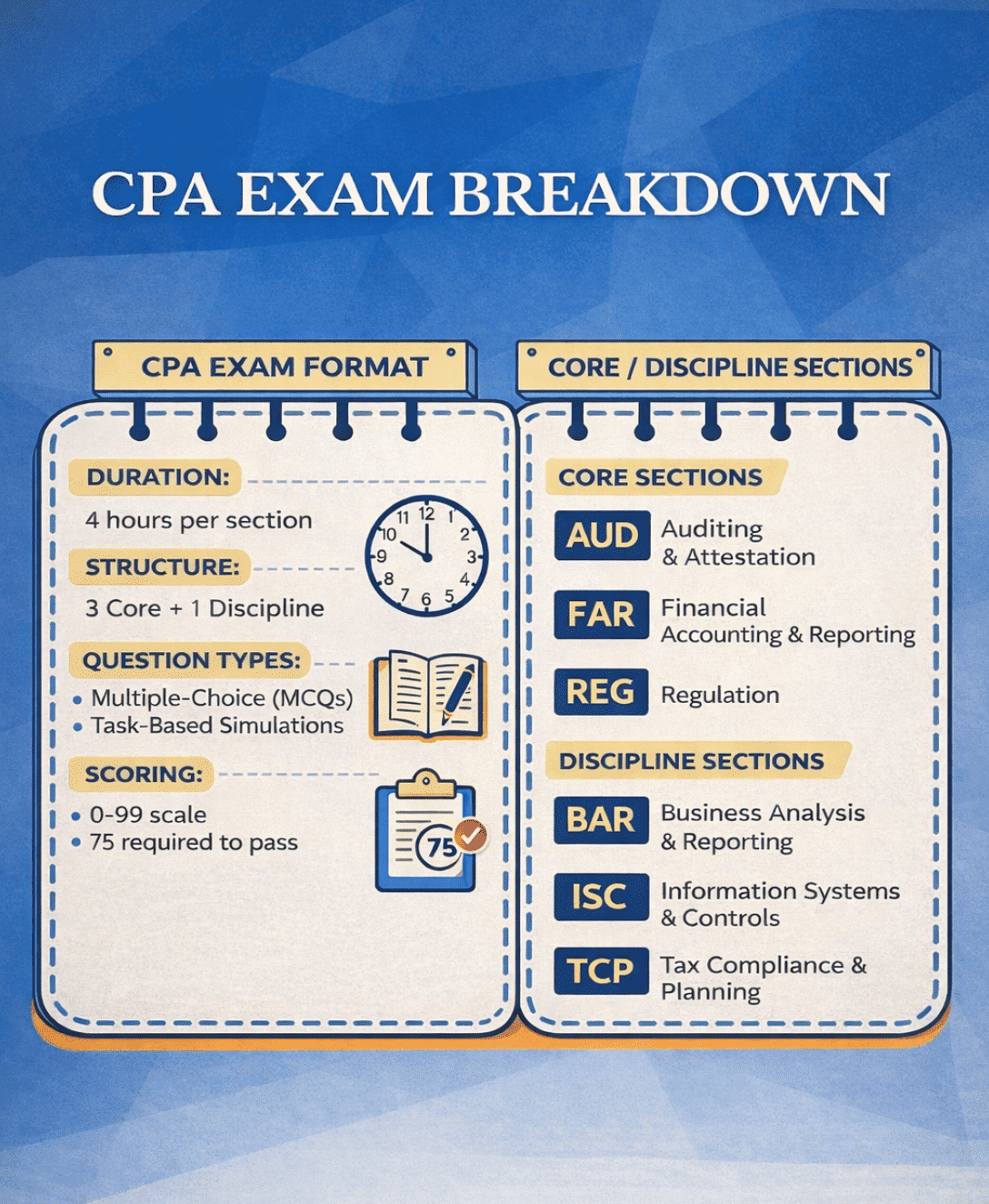

- Four Total Sections: The CPA exam includes three core sections (AUD, FAR, REG) and one discipline section (BAR, ISC, or TCP).

- Four-Hour Format: Each section lasts four hours and includes MCQs and task-based simulations.

- Core Sections Are Required: Every candidate must pass AUD, FAR, and REG.

- One Discipline Section: Choose BAR, ISC, or TCP based on your strengths and career goals.

- Practice Improves Performance: Consistent exposure to exam-style questions strengthens accuracy and confidence.

CPA Exam: Format & Timing

- Duration: Each CPA exam section is four hours.

- Structure: Three core sections plus one chosen discipline section.

- Question Types: Multiple-choice questions and task-based simulations.

- Scoring: Each section is scored from 0–99. A 75 is required to pass.

CPA Section Breakdown

Questions are grouped by section below. The core sections include more questions since every candidate must take them. The discipline sections include fewer questions, so you can focus on the one you plan to sit for.

Core Sections

- AUD (Auditing & Attestation): Auditing procedures, controls, evidence, reporting, and ethics.

- FAR (Financial Accounting & Reporting): Financial reporting standards and complex accounting transactions.

- REG (Regulation): Federal taxation, business law, and professional responsibilities.

Discipline Sections

- BAR (Business Analysis & Reporting): Advanced reporting and financial analysis.

- ISC (Information Systems & Controls): Information systems, controls, and assurance concepts.

- TCP (Tax Compliance & Planning): Advanced tax compliance and planning strategy.

Sample Test Questions:

1. AUD (Auditing & Attestation)

Question 1 (Easy)

Which of the following best describes the auditor’s responsibility regarding internal control in a financial statement audit?

A) To provide absolute assurance that no material weaknesses exist

B) To express an opinion on the effectiveness of internal control in all audits

C) To obtain an understanding of internal control sufficient to assess risks of material misstatement

D) To design controls for management to prevent fraud

Answer: C

Question 2 (Easy)

Which factor most directly affects the auditor’s assessment of inherent risk?

A) The effectiveness of internal controls

B) The complexity of the client’s transactions

C) The acceptable level of detection risk

D) The size of the audit firm

Answer: B

Question 3 (Moderate)

A CPA is asked to reissue an auditor’s report on prior-year financial statements. Before reissuing the report, the CPA should:

A) Obtain a new management representation letter

B) Perform additional audit procedures on current-year financial statements

C) Inquire whether subsequent events have occurred that would affect the prior financial statements

D) Reconfirm significant account balances

Answer: C

Question 4 (Moderate)

An auditor traces recorded sales transactions to shipping documents and customer orders. This procedure primarily tests which assertion?

A) Completeness

B) Existence

C) Rights and obligations

D) Presentation and disclosure

Answer: B

Question 5 (Moderate)

An auditor identifies a material misstatement that is not pervasive to the financial statements. The appropriate opinion is:

A) Unmodified

B) Qualified

C) Adverse

D) Disclaimer

Answer: B

Question 6 (Moderate)

A CPA discovers a significant deficiency in internal control. The CPA must:

A) Disclose it publicly in the auditor’s report

B) Communicate it in writing to management and those charged with governance

C) Withdraw from the engagement

D) Notify regulatory authorities

Answer: B

Question 7 (Hard)

After issuing a report, a CPA becomes aware of facts that existed at the report date and would have affected the opinion. Management refuses to revise the statements. The CPA should:

A) Take no action

B) Notify management and those charged with governance and seek to prevent reliance on the statements

C) Issue a new report dated as of discovery

D) Automatically withdraw

Answer: B

Question 8 (Hard)

If an auditor plans to reduce substantive testing by relying on internal controls, the auditor must perform:

A) Analytical procedures only

B) Tests of controls

C) Additional inquiry of management

D) Confirmation of all significant balances

Answer: B

2. FAR (Financial Accounting & Reporting)

Question 1 (Easy)

Which financial statement reports revenues and expenses for a specific period?

A) Balance sheet

B) Statement of cash flows

C) Income statement

D) Statement of retained earnings

Answer: C

Question 2 (Easy)

A company receives $24,000 on December 1 for services to be performed evenly over six months. How much revenue should be recognized in December?

A) $0

B) $4,000

C) $12,000

D) $24,000

Answer: B

Question 3 (Moderate)

On January 1, a company issued $100,000 of 6% bonds at 98. The bonds mature in five years and pay interest annually. Using the straight-line method, what is the Year 1 interest expense?

A) $6,000

B) $6,200

C) $6,400

D) $6,800

Answer: C

($2,000 discount ÷ 5 = $400; $6,000 + $400 = $6,400)

Question 4 (Moderate)

A company purchased equipment for $50,000 with a five-year useful life and no salvage value. What is annual straight-line depreciation?

A) $5,000

B) $8,000

C) $10,000

D) $12,500

Answer: C

Question 5 (Moderate)

A company reports net income of $120,000. Accounts receivable increased by $15,000, and accounts payable increased by $10,000. What is net cash provided by operating activities using the indirect method?

A) $115,000

B) $125,000

C) $130,000

D) $145,000

Answer: A

(120,000 − 15,000 + 10,000 = 115,000)

Question 6 (Moderate)

Inventory costing $40,000 has a market value of $35,000. Under lower-of-cost-or-market, what amount is reported?

A) $40,000

B) $37,500

C) $35,000

D) $30,000

Answer: C

Question 7 (Hard)

A material prior-year error understated depreciation expense by $20,000. How should the correction be reported?

A) As part of current-year income

B) As an extraordinary item

C) As a prior-period adjustment to beginning retained earnings

D) No correction required

Answer: C

Question 8 (Hard)

A finance lease has a present value of $200,000. A $50,000 payment is made at year-end, of which $15,000 is interest. What amount reduces the lease liability?

A) $50,000

B) $35,000

C) $15,000

D) $200,000

Answer: B

3. REG (Regulation)

Question 1 (Easy)

Which filing status generally provides the highest standard deduction?

A) Single

B) Married filing separately

C) Married filing jointly

D) Head of household

Answer: C

Question 2 (Easy)

Which element is required for a legally binding contract?

A) Written documentation

B) Notarization

C) Mutual assent and consideration

D) Witness signatures

Answer: C

Question 3 (Moderate)

An individual sells stock for $30,000. The stock was purchased for $18,000 and held for more than one year. How is the gain characterized?

A) $12,000 ordinary income

B) $12,000 short-term capital gain

C) $12,000 long-term capital gain

D) $30,000 long-term capital gain

Answer: C

Question 4 (Moderate)

A taxpayer contributes property with a basis of $20,000 and a fair market value of $28,000 to a qualified charity. Assuming no limitations, what is the deductible amount?

A) $20,000

B) $24,000

C) $28,000

D) $8,000

Answer: C

Question 5 (Moderate)

What is the current federal corporate income tax rate for C corporations?

A) Graduated rates

B) 21% flat rate

C) 25% flat rate

D) 28% flat rate

Answer: B

Question 6 (Moderate)

Under Circular 230, if a CPA discovers an error on a previously filed tax return, the CPA should:

A) Notify the IRS immediately

B) Inform the client of the error and potential consequences

C) Correct the return without client consent

D) Withdraw automatically

Answer: B

Question 7 (Hard)

A taxpayer exchanges business equipment (basis $40,000; FMV $55,000) for similar equipment valued at $50,000 and receives $5,000 cash. What gain is recognized?

A) $0

B) $5,000

C) $10,000

D) $15,000

Answer: B

Question 8 (Hard)

An S corporation distributes property (FMV $30,000; basis $18,000). What gain must the corporation recognize?

A) $0

B) $12,000

C) $18,000

D) $30,000

Answer: B

4. ISC (Information Systems & Controls)

Question 1 (Easy)

Which control helps prevent unauthorized system access?

A) Bank reconciliation

B) Segregation of duties

C) Multi-factor authentication

D) Exception report review

Answer: C

Question 2 (Moderate)

Which report provides assurance that a service organization’s controls operated effectively over time?

A) SOC 1 Type 1

B) SOC 1 Type 2

C) SOC 2 Type 1

D) SOC 3

Answer: B

Question 3 (Moderate)

An automated control prevents duplicate invoice payments. What risk is primarily addressed?

A) Data loss

B) Unauthorized access

C) Overstatement of expenses

D) Incomplete audit trail

Answer: C

Question 4 (Hard)

Which provides the strongest evidence that unauthorized program changes did not occur?

A) Inquiry of IT personnel

B) Review of access logs

C) Inspection of formal change approvals and independent testing documentation

D) Observation of system backups

Answer: C

5. BAR (Business Analysis & Reporting)

Question 1 (Easy)

Which ratio measures short-term liquidity?

A) Debt-to-equity

B) Current ratio

C) Return on assets

D) Gross margin

Answer: B

Question 2 (Moderate)

Net income is $200,000. Depreciation is $30,000. Inventory increased by $25,000. Accounts payable increasedby $10,0000. What is operating cash flow (indirect method)?

A) $185,000

B) $195,000

C) $205,000

D) $215,000

Answer: D

(200,000 + 30,000 − 25,000 + 10,000 = 215,000)

Question 3 (Moderate)

If two mutually exclusive projects have different IRRs and NPVs, which metric should generally be prioritized?

A) IRR

B) Payback period

C) NPV

D) Accounting rate of return

Answer: C

Question 4 (Hard)

A reporting unit has a carrying amount of $900,000, including goodwill of $200,000. Its fair value is $820,000. What goodwill impairment is recognized?

A) $0

B) $80,000

C) $100,000

D) $200,000

Answer: B

6. TCP (Tax Compliance & Planning)

Question 1 (Easy)

Which entity is generally treated as a pass-through for federal income tax purposes?

A) C corporation

B) S corporation

C) Publicly traded corporation

D) Personal service corporation

Answer: B

Question 2 (Moderate)

Self-employment tax is calculated on what portion of net earnings?

A) 100%

B) 92.35%

C) 75%

D) Adjusted gross income

Answer: B

Question 3 (Moderate)

An S corporation distribution exceeds a shareholder’s stock basis. The excess is treated as:

A) Ordinary income

B) Dividend income

C) Capital gain

D) Tax-free return of capital

Answer: C

Question 4 (Hard)

A taxpayer transfers property (FMV $60,000; basis $25,000) to a newly formed corporation for 100% of its stock under §351. What gain is recognized?

A) $0

B) $25,000

C) $35,000

D) $60,000

Answer: A

Final Thoughts

The biggest difference between passive studying and real readiness is applying what you know under exam-style conditions. That’s why I built this set to reflect the structure, pacing, and difficulty you’ll actually face.

You can use these questions to test your preparation honestly, identify weak areas, and adjust your study plan. Many candidates benefit from practicing with realistic questions consistently, whether that’s through independent sets like this or one of the top CPA prep courses that mirror the actual exam. The key is steady, intentional practice that builds confidence before test day.

FAQs

CPA exam practice questions help you apply concepts in financial accounting, auditing, tax compliance, and information systems. They help you identify areas of weakness, track progress, and improve readiness before exam day.

Yes. These realistic multiple-choice questions (MCQs) follow the format used on each CPA exam section. They prepare you for both MCQs and task-based simulations on the test day.

Focus first on the CPA exam section you’re currently studying for (AUD, FAR, REG, BAR, ISC, or TCP). Targeted practice helps improve preparation and builds confidence before test day.

Each CPA exam section is four hours long and includes multiple-choice questions and task-based simulations. You must complete all parts within the allotted time to receive a score.

Treat these sample questions like a mini test. Track results, review weak areas, and focus your study where improvement is needed to increase your chances of passing.